https://energyeducation.ca/encyclopedia/Joule

Yes and since 2019 we have gained about 5 inches of soil.

If you frost cupcakes for 2 hours for couple day in a bakery you counted fully employed.

As we seen Mr. Bond will decide to bitch slap Mr. Market later than sooner.

https://www.youtube.com/watch?v=F2HH7J-Sx80

http://gdxforum.com/forum/download/file.php?id=76 swamp disease and the gold coin on ahabs main mast

https://www.nber.org/system/files/worki ... w26943.pdf

The Murder-Suicide of the Rentier: Population Aging and the Risk Premium.

The ERP as discussed, and some here see as the GATT matter of fact as SOE eliminates impediment's to the glorious

SOS dialectic that will be channeled as we see in real time.

The fourth-step framework for ideological subversion on the national scale in active measures.

Effective cannot be ignored since let us know when the GOP has a pulse.

We are rather as degeneracy or as we seen regeneracy imposition of terms.

Goes back to DCF and the demise of the middle being ground to dust from the wasting intent.

Higgenbotham's Dark Age Hovel

Re: Higgenbotham's Dark Age Hovel

Last edited by aeden on Thu May 02, 2024 3:55 pm, edited 1 time in total.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

https://www.ecosophia.net/lenocracy-in- ... ublishing/All this calls to mind one of the writers whose work has been central to my blogging since its earliest days, English historian Arnold Toynbee. As my regular readers will doubtless remember, Toynbee lived in Britain in the twentieth century, and so he was understandably interested in the reasons why empires fall. He devoted most of his working life to a sprawling twelve-volume study of that question, which he titled simply A Study of History.

His explanation for the decline and fall of civilizations was subtle but straightforward. He noted that most fallen empires could have recovered from the crises that destroyed them, but reliably failed to take the steps that could have saved them or at least prolonged their existence. In his phrasing, if civilizations had death certificates, the cause of death listed wouldn’t be accident or murder, it would be suicide. A close examination of the politics of failing societies led him to see a crucial change in their leadership as the deciding factor. Societies grow and thrive when their governing classes are able to come up with new and effective responses to the crises history throws at them. Toynbee called such a governing class a creative minority, and talked about the way that its successes inspired the loyalty and trust of the rest of the population.

Societies decay and die, in turn, when a formerly creative minority loses its willingness to respond to a changing world, and becomes more interested in shielding its members from the consequences of failure than in finding new ways to succeed. Such a class becomes a dominant minority, in Toynbee’s terms. Since it can no longer inspire loyalty and trust, it turns to bribery, coercion, and sheer institutional inertia to maintain its control over the society it once led and now merely exploits. Once a dominant minority has stopped coming up with effective solutions to the problems its society faces, of course, those problems go unsolved, and eventually bring the society crashing down.

That’s what we’re seeing in microcosm in the publishing industry today. We may not be too far from the point when venture capitalists, the scavenging jackals of our lenocratic society, drag down the big publishing combines, tear them apart, feast on what remains of their flesh, and leave the bones to dry in the sun, clearing a space in which smaller and less inept firms can expand to fill the void. What greater jackals might be patiently following the society of which the big publishing firms are a microcosm, waiting for a similar moment, is a question we’ll save for another time.

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

I'll spend a few posts discussing Greer's analysis above. It was Ben Bernanke who gave the dominant minority, as Greer refers to it, the ability to fully take charge.

This article is nine years old.Higgenbotham wrote: ↑Mon Sep 26, 2022 10:50 amBernanke put the process of sucking the periphery dry into hyperdrive with QE. I also had in mind that the periphery includes parts of the US as well as the rest of the world.

https://www.independent.co.uk/news/busi ... rnalSearchBen Bernanke joins Citadel hedge fund

He will offer analysis on economic and financial issues

Ben Chu

Friday 17 April 2015 07:58 BST

Ben Bernanke, the former president of America’s central bank, is to become a senior adviser to one of the world’s largest hedge funds, raising fresh concerns about the “revolving door” between Washington and Wall Street.

The former Federal Reserve president, who left his post in January 2014, is to join Ken Griffin’s Citadel Investment, where he will offer analysis on economic and financial issues to the $25bn (£17bn) fund’s investment committees as well as meeting the Fund’s investors.

He is the latest in a long line of financial regulators and public officials to join the world of asset management. Mr Bernanke’s predecessor, Alan Greenspan, joined Paulson & Co in 2008 as an advisor, two years after leaving the Federal Reserve. The former US Treasury Secretary Larry Summers worked for D E Shaw as a part-time managing partner in 2006. More recently Jeremy C Stein, a former Fed governor, joined BlueMountain Capital Management as a consultant.

Mr Bernanke told the New York Times that he was sensitive towards public concerns about the interchange between public officials and Wall Street but insisted his new job was not a conflict of interest.

Mr Bernanke did not disclose what he will be paid by Citadel but he said he would be paid an annual fee, would not own a stake in the firm and would receive no bonus.

Mr Bernanke’s move also raised eyebrows because Citadel is one of the most leveraged of the world’s major hedge funds. Citadel is also involved in high-frequency trading, which has drawn criticism for unfairly disadvantaging ordinary investors.

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

Remarks by Governor Ben S. Bernanke

Before the National Economists Club, Washington, D.C.

November 21, 2002

Deflation: Making Sure "It" Doesn't Happen Here

Since World War II, inflation--the apparently inexorable rise in the prices of goods and services--has been the bane of central bankers. Economists of various stripes have argued that inflation is the inevitable result of (pick your favorite) the abandonment of metallic monetary standards, a lack of fiscal discipline, shocks to the price of oil and other commodities, struggles over the distribution of income, excessive money creation, self-confirming inflation expectations, an "inflation bias" in the policies of central banks, and still others. Despite widespread "inflation pessimism," however, during the 1980s and 1990s most industrial-country central banks were able to cage, if not entirely tame, the inflation dragon. Although a number of factors converged to make this happy outcome possible, an essential element was the heightened understanding by central bankers and, equally as important, by political leaders and the public at large of the very high costs of allowing the economy to stray too far from price stability.

With inflation rates now quite low in the United States, however, some have expressed concern that we may soon face a new problem--the danger of deflation, or falling prices. That this concern is not purely hypothetical is brought home to us whenever we read newspaper reports about Japan, where what seems to be a relatively moderate deflation--a decline in consumer prices of about 1 percent per year--has been associated with years of painfully slow growth, rising joblessness, and apparently intractable financial problems in the banking and corporate sectors. While it is difficult to sort out cause from effect, the consensus view is that deflation has been an important negative factor in the Japanese slump.

So, is deflation a threat to the economic health of the United States? Not to leave you in suspense, I believe that the chance of significant deflation in the United States in the foreseeable future is extremely small, for two principal reasons. The first is the resilience and structural stability of the U.S. economy itself. Over the years, the U.S. economy has shown a remarkable ability to absorb shocks of all kinds, to recover, and to continue to grow. Flexible and efficient markets for labor and capital, an entrepreneurial tradition, and a general willingness to tolerate and even embrace technological and economic change all contribute to this resiliency. A particularly important protective factor in the current environment is the strength of our financial system: Despite the adverse shocks of the past year, our banking system remains healthy and well-regulated, and firm and household balance sheets are for the most part in good shape. Also helpful is that inflation has recently been not only low but quite stable, with one result being that inflation expectations seem well anchored. For example, according to the University of Michigan survey that underlies the index of consumer sentiment, the median expected rate of inflation during the next five to ten years among those interviewed was 2.9 percent in October 2002, as compared with 2.7 percent a year earlier and 3.0 percent two years earlier--a stable record indeed.

The second bulwark against deflation in the United States, and the one that will be the focus of my remarks today, is the Federal Reserve System itself. The Congress has given the Fed the responsibility of preserving price stability (among other objectives), which most definitely implies avoiding deflation as well as inflation. I am confident that the Fed would take whatever means necessary to prevent significant deflation in the United States and, moreover, that the U.S. central bank, in cooperation with other parts of the government as needed, has sufficient policy instruments to ensure that any deflation that might occur would be both mild and brief.

Of course, we must take care lest confidence become over-confidence. Deflationary episodes are rare, and generalization about them is difficult. Indeed, a recent Federal Reserve study of the Japanese experience concluded that the deflation there was almost entirely unexpected, by both foreign and Japanese observers alike (Ahearne et al., 2002). So, having said that deflation in the United States is highly unlikely, I would be imprudent to rule out the possibility altogether. Accordingly, I want to turn to a further exploration of the causes of deflation, its economic effects, and the policy instruments that can be deployed against it. Before going further I should say that my comments today reflect my own views only and are not necessarily those of my colleagues on the Board of Governors or the Federal Open Market Committee.

Deflation: Its Causes and Effects

Deflation is defined as a general decline in prices, with emphasis on the word "general." At any given time, especially in a low-inflation economy like that of our recent experience, prices of some goods and services will be falling. Price declines in a specific sector may occur because productivity is rising and costs are falling more quickly in that sector than elsewhere or because the demand for the output of that sector is weak relative to the demand for other goods and services. Sector-specific price declines, uncomfortable as they may be for producers in that sector, are generally not a problem for the economy as a whole and do not constitute deflation. Deflation per se occurs only when price declines are so widespread that broad-based indexes of prices, such as the consumer price index, register ongoing declines.

The sources of deflation are not a mystery. Deflation is in almost all cases a side effect of a collapse of aggregate demand--a drop in spending so severe that producers must cut prices on an ongoing basis in order to find buyers.1 Likewise, the economic effects of a deflationary episode, for the most part, are similar to those of any other sharp decline in aggregate spending--namely, recession, rising unemployment, and financial stress.

However, a deflationary recession may differ in one respect from "normal" recessions in which the inflation rate is at least modestly positive: Deflation of sufficient magnitude may result in the nominal interest rate declining to zero or very close to zero.2 Once the nominal interest rate is at zero, no further downward adjustment in the rate can occur, since lenders generally will not accept a negative nominal interest rate when it is possible instead to hold cash. At this point, the nominal interest rate is said to have hit the "zero bound."

Deflation great enough to bring the nominal interest rate close to zero poses special problems for the economy and for policy. First, when the nominal interest rate has been reduced to zero, the real interest rate paid by borrowers equals the expected rate of deflation, however large that may be.3 To take what might seem like an extreme example (though in fact it occurred in the United States in the early 1930s), suppose that deflation is proceeding at a clip of 10 percent per year. Then someone who borrows for a year at a nominal interest rate of zero actually faces a 10 percent real cost of funds, as the loan must be repaid in dollars whose purchasing power is 10 percent greater than that of the dollars borrowed originally. In a period of sufficiently severe deflation, the real cost of borrowing becomes prohibitive. Capital investment, purchases of new homes, and other types of spending decline accordingly, worsening the economic downturn.

Although deflation and the zero bound on nominal interest rates create a significant problem for those seeking to borrow, they impose an even greater burden on households and firms that had accumulated substantial debt before the onset of the deflation. This burden arises because, even if debtors are able to refinance their existing obligations at low nominal interest rates, with prices falling they must still repay the principal in dollars of increasing (perhaps rapidly increasing) real value. When William Jennings Bryan made his famous "cross of gold" speech in his 1896 presidential campaign, he was speaking on behalf of heavily mortgaged farmers whose debt burdens were growing ever larger in real terms, the result of a sustained deflation that followed America's post-Civil-War return to the gold standard.4 The financial distress of debtors can, in turn, increase the fragility of the nation's financial system--for example, by leading to a rapid increase in the share of bank loans that are delinquent or in default. Japan in recent years has certainly faced the problem of "debt-deflation"--the deflation-induced, ever-increasing real value of debts. Closer to home, massive financial problems, including defaults, bankruptcies, and bank failures, were endemic in America's worst encounter with deflation, in the years 1930-33--a period in which (as I mentioned) the U.S. price level fell about 10 percent per year.

Beyond its adverse effects in financial markets and on borrowers, the zero bound on the nominal interest rate raises another concern--the limitation that it places on conventional monetary policy. Under normal conditions, the Fed and most other central banks implement policy by setting a target for a short-term interest rate--the overnight federal funds rate in the United States--and enforcing that target by buying and selling securities in open capital markets. When the short-term interest rate hits zero, the central bank can no longer ease policy by lowering its usual interest-rate target.5

Because central banks conventionally conduct monetary policy by manipulating the short-term nominal interest rate, some observers have concluded that when that key rate stands at or near zero, the central bank has "run out of ammunition"--that is, it no longer has the power to expand aggregate demand and hence economic activity. It is true that once the policy rate has been driven down to zero, a central bank can no longer use its traditional means of stimulating aggregate demand and thus will be operating in less familiar territory. The central bank's inability to use its traditional methods may complicate the policymaking process and introduce uncertainty in the size and timing of the economy's response to policy actions. Hence I agree that the situation is one to be avoided if possible.

However, a principal message of my talk today is that a central bank whose accustomed policy rate has been forced down to zero has most definitely not run out of ammunition. As I will discuss, a central bank, either alone or in cooperation with other parts of the government, retains considerable power to expand aggregate demand and economic activity even when its accustomed policy rate is at zero. In the remainder of my talk, I will first discuss measures for preventing deflation--the preferable option if feasible. I will then turn to policy measures that the Fed and other government authorities can take if prevention efforts fail and deflation appears to be gaining a foothold in the economy.

Preventing Deflation

As I have already emphasized, deflation is generally the result of low and falling aggregate demand. The basic prescription for preventing deflation is therefore straightforward, at least in principle: Use monetary and fiscal policy as needed to support aggregate spending, in a manner as nearly consistent as possible with full utilization of economic resources and low and stable inflation. In other words, the best way to get out of trouble is not to get into it in the first place. Beyond this commonsense injunction, however, there are several measures that the Fed (or any central bank) can take to reduce the risk of falling into deflation.

First, the Fed should try to preserve a buffer zone for the inflation rate, that is, during normal times it should not try to push inflation down all the way to zero.6 Most central banks seem to understand the need for a buffer zone. For example, central banks with explicit inflation targets almost invariably set their target for inflation above zero, generally between 1 and 3 percent per year. Maintaining an inflation buffer zone reduces the risk that a large, unanticipated drop in aggregate demand will drive the economy far enough into deflationary territory to lower the nominal interest rate to zero. Of course, this benefit of having a buffer zone for inflation must be weighed against the costs associated with allowing a higher inflation rate in normal times.

Second, the Fed should take most seriously--as of course it does--its responsibility to ensure financial stability in the economy. Irving Fisher (1933) was perhaps the first economist to emphasize the potential connections between violent financial crises, which lead to "fire sales" of assets and falling asset prices, with general declines in aggregate demand and the price level. A healthy, well capitalized banking system and smoothly functioning capital markets are an important line of defense against deflationary shocks. The Fed should and does use its regulatory and supervisory powers to ensure that the financial system will remain resilient if financial conditions change rapidly. And at times of extreme threat to financial stability, the Federal Reserve stands ready to use the discount window and other tools to protect the financial system, as it did during the 1987 stock market crash and the September 11, 2001, terrorist attacks.

Third, as suggested by a number of studies, when inflation is already low and the fundamentals of the economy suddenly deteriorate, the central bank should act more preemptively and more aggressively than usual in cutting rates (Orphanides and Wieland, 2000; Reifschneider and Williams, 2000; Ahearne et al., 2002). By moving decisively and early, the Fed may be able to prevent the economy from slipping into deflation, with the special problems that entails.

As I have indicated, I believe that the combination of strong economic fundamentals and policymakers that are attentive to downside as well as upside risks to inflation make significant deflation in the United States in the foreseeable future quite unlikely. But suppose that, despite all precautions, deflation were to take hold in the U.S. economy and, moreover, that the Fed's policy instrument--the federal funds rate--were to fall to zero. What then? In the remainder of my talk I will discuss some possible options for stopping a deflation once it has gotten under way. I should emphasize that my comments on this topic are necessarily speculative, as the modern Federal Reserve has never faced this situation nor has it pre-committed itself formally to any specific course of action should deflation arise. Furthermore, the specific responses the Fed would undertake would presumably depend on a number of factors, including its assessment of the whole range of risks to the economy and any complementary policies being undertaken by other parts of the U.S. government.7

Curing Deflation

Let me start with some general observations about monetary policy at the zero bound, sweeping under the rug for the moment some technical and operational issues.

As I have mentioned, some observers have concluded that when the central bank's policy rate falls to zero--its practical minimum--monetary policy loses its ability to further stimulate aggregate demand and the economy. At a broad conceptual level, and in my view in practice as well, this conclusion is clearly mistaken. Indeed, under a fiat (that is, paper) money system, a government (in practice, the central bank in cooperation with other agencies) should always be able to generate increased nominal spending and inflation, even when the short-term nominal interest rate is at zero.

The conclusion that deflation is always reversible under a fiat money system follows from basic economic reasoning. A little parable may prove useful: Today an ounce of gold sells for $300, more or less. Now suppose that a modern alchemist solves his subject's oldest problem by finding a way to produce unlimited amounts of new gold at essentially no cost. Moreover, his invention is widely publicized and scientifically verified, and he announces his intention to begin massive production of gold within days. What would happen to the price of gold? Presumably, the potentially unlimited supply of cheap gold would cause the market price of gold to plummet. Indeed, if the market for gold is to any degree efficient, the price of gold would collapse immediately after the announcement of the invention, before the alchemist had produced and marketed a single ounce of yellow metal.

What has this got to do with monetary policy? Like gold, U.S. dollars have value only to the extent that they are strictly limited in supply. But the U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so, the U.S. government can also reduce the value of a dollar in terms of goods and services, which is equivalent to raising the prices in dollars of those goods and services. We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation.

Of course, the U.S. government is not going to print money and distribute it willy-nilly (although as we will see later, there are practical policies that approximate this behavior).8 Normally, money is injected into the economy through asset purchases by the Federal Reserve. To stimulate aggregate spending when short-term interest rates have reached zero, the Fed must expand the scale of its asset purchases or, possibly, expand the menu of assets that it buys. Alternatively, the Fed could find other ways of injecting money into the system--for example, by making low-interest-rate loans to banks or cooperating with the fiscal authorities. Each method of adding money to the economy has advantages and drawbacks, both technical and economic. One important concern in practice is that calibrating the economic effects of nonstandard means of injecting money may be difficult, given our relative lack of experience with such policies. Thus, as I have stressed already, prevention of deflation remains preferable to having to cure it. If we do fall into deflation, however, we can take comfort that the logic of the printing press example must assert itself, and sufficient injections of money will ultimately always reverse a deflation.

So what then might the Fed do if its target interest rate, the overnight federal funds rate, fell to zero? One relatively straightforward extension of current procedures would be to try to stimulate spending by lowering rates further out along the Treasury term structure--that is, rates on government bonds of longer maturities.9 There are at least two ways of bringing down longer-term rates, which are complementary and could be employed separately or in combination. One approach, similar to an action taken in the past couple of years by the Bank of Japan, would be for the Fed to commit to holding the overnight rate at zero for some specified period. Because long-term interest rates represent averages of current and expected future short-term rates, plus a term premium, a commitment to keep short-term rates at zero for some time--if it were credible--would induce a decline in longer-term rates. A more direct method, which I personally prefer, would be for the Fed to begin announcing explicit ceilings for yields on longer-maturity Treasury debt (say, bonds maturing within the next two years). The Fed could enforce these interest-rate ceilings by committing to make unlimited purchases of securities up to two years from maturity at prices consistent with the targeted yields. If this program were successful, not only would yields on medium-term Treasury securities fall, but (because of links operating through expectations of future interest rates) yields on longer-term public and private debt (such as mortgages) would likely fall as well.

Lower rates over the maturity spectrum of public and private securities should strengthen aggregate demand in the usual ways and thus help to end deflation. Of course, if operating in relatively short-dated Treasury debt proved insufficient, the Fed could also attempt to cap yields of Treasury securities at still longer maturities, say three to six years. Yet another option would be for the Fed to use its existing authority to operate in the markets for agency debt (for example, mortgage-backed securities issued by Ginnie Mae, the Government National Mortgage Association).

Historical experience tends to support the proposition that a sufficiently determined Fed can peg or cap Treasury bond prices and yields at other than the shortest maturities. The most striking episode of bond-price pegging occurred during the years before the Federal Reserve-Treasury Accord of 1951.10 Prior to that agreement, which freed the Fed from its responsibility to fix yields on government debt, the Fed maintained a ceiling of 2-1/2 percent on long-term Treasury bonds for nearly a decade. Moreover, it simultaneously established a ceiling on the twelve-month Treasury certificate of between 7/8 percent to 1-1/4 percent and, during the first half of that period, a rate of 3/8 percent on the 90-day Treasury bill. The Fed was able to achieve these low interest rates despite a level of outstanding government debt (relative to GDP) significantly greater than we have today, as well as inflation rates substantially more variable. At times, in order to enforce these low rates, the Fed had actually to purchase the bulk of outstanding 90-day bills. Interestingly, though, the Fed enforced the 2-1/2 percent ceiling on long-term bond yields for nearly a decade without ever holding a substantial share of long-maturity bonds outstanding.11 For example, the Fed held 7.0 percent of outstanding Treasury securities in 1945 and 9.2 percent in 1951 (the year of the Accord), almost entirely in the form of 90-day bills. For comparison, in 2001 the Fed held 9.7 percent of the stock of outstanding Treasury debt.

To repeat, I suspect that operating on rates on longer-term Treasuries would provide sufficient leverage for the Fed to achieve its goals in most plausible scenarios. If lowering yields on longer-dated Treasury securities proved insufficient to restart spending, however, the Fed might next consider attempting to influence directly the yields on privately issued securities. Unlike some central banks, and barring changes to current law, the Fed is relatively restricted in its ability to buy private securities directly.12 However, the Fed does have broad powers to lend to the private sector indirectly via banks, through the discount window.13 Therefore a second policy option, complementary to operating in the markets for Treasury and agency debt, would be for the Fed to offer fixed-term loans to banks at low or zero interest, with a wide range of private assets (including, among others, corporate bonds, commercial paper, bank loans, and mortgages) deemed eligible as collateral.14 For example, the Fed might make 90-day or 180-day zero-interest loans to banks, taking corporate commercial paper of the same maturity as collateral. Pursued aggressively, such a program could significantly reduce liquidity and term premiums on the assets used as collateral. Reductions in these premiums would lower the cost of capital both to banks and the nonbank private sector, over and above the beneficial effect already conferred by lower interest rates on government securities.15

The Fed can inject money into the economy in still other ways. For example, the Fed has the authority to buy foreign government debt, as well as domestic government debt. Potentially, this class of assets offers huge scope for Fed operations, as the quantity of foreign assets eligible for purchase by the Fed is several times the stock of U.S. government debt.16

I need to tread carefully here. Because the economy is a complex and interconnected system, Fed purchases of the liabilities of foreign governments have the potential to affect a number of financial markets, including the market for foreign exchange. In the United States, the Department of the Treasury, not the Federal Reserve, is the lead agency for making international economic policy, including policy toward the dollar; and the Secretary of the Treasury has expressed the view that the determination of the value of the U.S. dollar should be left to free market forces. Moreover, since the United States is a large, relatively closed economy, manipulating the exchange value of the dollar would not be a particularly desirable way to fight domestic deflation, particularly given the range of other options available. Thus, I want to be absolutely clear that I am today neither forecasting nor recommending any attempt by U.S. policymakers to target the international value of the dollar.

Although a policy of intervening to affect the exchange value of the dollar is nowhere on the horizon today, it's worth noting that there have been times when exchange rate policy has been an effective weapon against deflation. A striking example from U.S. history is Franklin Roosevelt's 40 percent devaluation of the dollar against gold in 1933-34, enforced by a program of gold purchases and domestic money creation. The devaluation and the rapid increase in money supply it permitted ended the U.S. deflation remarkably quickly. Indeed, consumer price inflation in the United States, year on year, went from -10.3 percent in 1932 to -5.1 percent in 1933 to 3.4 percent in 1934.17 The economy grew strongly, and by the way, 1934 was one of the best years of the century for the stock market. If nothing else, the episode illustrates that monetary actions can have powerful effects on the economy, even when the nominal interest rate is at or near zero, as was the case at the time of Roosevelt's devaluation.

Fiscal Policy

Each of the policy options I have discussed so far involves the Fed's acting on its own. In practice, the effectiveness of anti-deflation policy could be significantly enhanced by cooperation between the monetary and fiscal authorities. A broad-based tax cut, for example, accommodated by a program of open-market purchases to alleviate any tendency for interest rates to increase, would almost certainly be an effective stimulant to consumption and hence to prices. Even if households decided not to increase consumption but instead re-balanced their portfolios by using their extra cash to acquire real and financial assets, the resulting increase in asset values would lower the cost of capital and improve the balance sheet positions of potential borrowers. A money-financed tax cut is essentially equivalent to Milton Friedman's famous "helicopter drop" of money.18

Of course, in lieu of tax cuts or increases in transfers the government could increase spending on current goods and services or even acquire existing real or financial assets. If the Treasury issued debt to purchase private assets and the Fed then purchased an equal amount of Treasury debt with newly created money, the whole operation would be the economic equivalent of direct open-market operations in private assets.

Japan

The claim that deflation can be ended by sufficiently strong action has no doubt led you to wonder, if that is the case, why has Japan not ended its deflation? The Japanese situation is a complex one that I cannot fully discuss today. I will just make two brief, general points.

First, as you know, Japan's economy faces some significant barriers to growth besides deflation, including massive financial problems in the banking and corporate sectors and a large overhang of government debt. Plausibly, private-sector financial problems have muted the effects of the monetary policies that have been tried in Japan, even as the heavy overhang of government debt has made Japanese policymakers more reluctant to use aggressive fiscal policies (for evidence see, for example, Posen, 1998). Fortunately, the U.S. economy does not share these problems, at least not to anything like the same degree, suggesting that anti-deflationary monetary and fiscal policies would be more potent here than they have been in Japan.

Second, and more important, I believe that, when all is said and done, the failure to end deflation in Japan does not necessarily reflect any technical infeasibility of achieving that goal. Rather, it is a byproduct of a longstanding political debate about how best to address Japan's overall economic problems. As the Japanese certainly realize, both restoring banks and corporations to solvency and implementing significant structural change are necessary for Japan's long-run economic health. But in the short run, comprehensive economic reform will likely impose large costs on many, for example, in the form of unemployment or bankruptcy. As a natural result, politicians, economists, businesspeople, and the general public in Japan have sharply disagreed about competing proposals for reform. In the resulting political deadlock, strong policy actions are discouraged, and cooperation among policymakers is difficult to achieve.

In short, Japan's deflation problem is real and serious; but, in my view, political constraints, rather than a lack of policy instruments, explain why its deflation has persisted for as long as it has. Thus, I do not view the Japanese experience as evidence against the general conclusion that U.S. policymakers have the tools they need to prevent, and, if necessary, to cure a deflationary recession in the United States.

Conclusion

Sustained deflation can be highly destructive to a modern economy and should be strongly resisted. Fortunately, for the foreseeable future, the chances of a serious deflation in the United States appear remote indeed, in large part because of our economy's underlying strengths but also because of the determination of the Federal Reserve and other U.S. policymakers to act preemptively against deflationary pressures. Moreover, as I have discussed today, a variety of policy responses are available should deflation appear to be taking hold. Because some of these alternative policy tools are relatively less familiar, they may raise practical problems of implementation and of calibration of their likely economic effects. For this reason, as I have emphasized, prevention of deflation is preferable to cure. Nevertheless, I hope to have persuaded you that the Federal Reserve and other economic policymakers would be far from helpless in the face of deflation, even should the federal funds rate hit its zero bound.19

References

Ahearne, Alan, Joseph Gagnon, Jane Haltmaier, Steve Kamin, and others, "Preventing Deflation: Lessons from Japan's Experiences in the 1990s," Board of Governors, International Finance Discussion Paper No. 729, June 2002.

Clouse, James, Dale Henderson, Athanasios Orphanides, David Small, and Peter Tinsley, "Monetary Policy When the Nominal Short-term Interest Rate Is Zero," Board of Governors of the Federal Reserve System, Finance and Economics Discussion Series No. 2000-51, November 2000.

Eichengreen, Barry, and Peter M. Garber, "Before the Accord: U.S. Monetary-Financial Policy, 1945-51," in R. Glenn Hubbard, ed., Financial Markets and Financial Crises, Chicago: University of Chicago Press for NBER, 1991.

Eggertson, Gauti, "How to Fight Deflation in a Liquidity Trap: Committing to Being Irresponsible," unpublished paper, International Monetary Fund, October 2002.

Fisher, Irving, "The Debt-Deflation Theory of Great Depressions," Econometrica (March 1933) pp. 337-57.

Hetzel, Robert L. and Ralph F. Leach, "The Treasury-Fed Accord: A New Narrative Account," Federal Reserve Bank of Richmond, Economic Quarterly (Winter 2001) pp. 33-55.

Orphanides, Athanasios and Volker Wieland, "Efficient Monetary Design Near Price Stability," Journal of the Japanese and International Economies (2000) pp. 327-65.

Posen, Adam S., Restoring Japan's Economic Growth, Washington, D.C.: Institute for International Economics, 1998.

Reifschneider, David, and John C. Williams, "Three Lessons for Monetary Policy in a Low-Inflation Era," Journal of Money, Credit, and Banking (November 2000) Part 2 pp. 936-66.

Toma, Mark, "Interest Rate Controls: The United States in the 1940s," Journal of Economic History (September 1992) pp. 631-50.

Footnotes

1. Conceivably, deflation could also be caused by a sudden, large expansion in aggregate supply arising, for example, from rapid gains in productivity and broadly declining costs. I don't know of any unambiguous example of a supply-side deflation, although China in recent years is a possible case. Note that a supply-side deflation would be associated with an economic boom rather than a recession. Return to text

2. The nominal interest rate is the sum of the real interest rate and expected inflation. If expected inflation moves with actual inflation, and the real interest rate is not too variable, then the nominal interest rate declines when inflation declines--an effect known as the Fisher effect, after the early twentieth-century economist Irving Fisher. If the rate of deflation is equal to or greater than the real interest rate, the Fisher effect predicts that the nominal interest rate will equal zero. Return to text

3. The real interest rate equals the nominal interest rate minus the expected rate of inflation (see the previous footnote). The real interest rate measures the real (that is, inflation-adjusted) cost of borrowing or lending. Return to text

4. Throughout the latter part of the nineteenth century, a worldwide gold shortage was forcing down prices in all countries tied to the gold standard. Ironically, however, by the time that Bryan made his famous speech, a new cyanide-based method for extracting gold from ore had greatly increased world gold supplies, ending the deflationary pressure. Return to text

5. A rather different, but historically important, problem associated with the zero bound is the possibility that policymakers may mistakenly interpret the zero nominal interest rate as signaling conditions of "easy money." The Federal Reserve apparently made this error in the 1930s. In fact, when prices are falling, the real interest rate may be high and monetary policy tight, despite a nominal interest rate at or near zero. Return to text

6. Several studies have concluded that the measured rate of inflation overstates the "true" rate of inflation, because of several biases in standard price indexes that are difficult to eliminate in practice. The upward bias in the measurement of true inflation is another reason to aim for a measured inflation rate above zero. Return to text

7. See Clouse et al. (2000) for a more detailed discussion of monetary policy options when the nominal short-term interest rate is zero. Return to text

8. Keynes, however, once semi-seriously proposed, as an anti-deflationary measure, that the government fill bottles with currency and bury them in mine shafts to be dug up by the public. Return to text

9. Because the term structure is normally upward sloping, especially during periods of economic weakness, longer-term rates could be significantly above zero even when the overnight rate is at the zero bound. Return to text

10. S See Hetzel and Leach (2001) for a fascinating account of the events leading to the Accord. Return to text

11. See Eichengreen and Garber (1991) and Toma (1992) for descriptions and analyses of the pre-Accord period. Both articles conclude that the Fed's commitment to low inflation helped convince investors to hold long-term bonds at low rates in the 1940s and 1950s. (A similar dynamic would work in the Fed's favor today.) The rate-pegging policy finally collapsed because the money creation associated with buying Treasury securities was generating inflationary pressures. Of course, in a deflationary situation, generating inflationary pressure is precisely what the policy is trying to accomplish.

An episode apparently less favorable to the view that the Fed can manipulate Treasury yields was the so-called Operation Twist of the 1960s, during which an attempt was made to raise short-term yields and lower long-term yields simultaneously by selling at the short end and buying at the long end. Academic opinion on the effectiveness of Operation Twist is divided. In any case, this episode was rather small in scale, did not involve explicit announcement of target rates, and occurred when interest rates were not close to zero. Return to text

12. The Fed is allowed to buy certain short-term private instruments, such as bankers' acceptances, that are not much used today. It is also permitted to make IPC (individual, partnership, and corporation) loans directly to the private sector, but only under stringent criteria. This latter power has not been used since the Great Depression but could be invoked in an emergency deemed sufficiently serious by the Board of Governors. Return to text

13. Effective January 9, 2003, the discount window will be restructured into a so-called Lombard facility, from which well-capitalized banks will be able to borrow freely at a rate above the federal funds rate. These changes have no important bearing on the present discussion. Return to text

14. By statute, the Fed has considerable leeway to determine what assets to accept as collateral. Return to text

15. In carrying out normal discount window operations, the Fed absorbs virtually no credit risk because the borrowing bank remains responsible for repaying the discount window loan even if the issuer of the asset used as collateral defaults. Hence both the private issuer of the asset and the bank itself would have to fail nearly simultaneously for the Fed to take a loss. The fact that the Fed bears no credit risk places a limit on how far down the Fed can drive the cost of capital to private nonbank borrowers. For various reasons the Fed might well be reluctant to incur credit risk, as would happen if it bought assets directly from the private nonbank sector. However, should this additional measure become necessary, the Fed could of course always go to the Congress to ask for the requisite powers to buy private assets. The Fed also has emergency powers to make loans to the private sector (see footnote 12), which could be brought to bear if necessary. Return to text

16. The Fed has committed to the Congress that it will not use this power to "bail out" foreign governments; hence in practice it would purchase only highly rated foreign government debt. Return to text

17. U.S. Bureau of the Census, Historical Statistics of the United States, Colonial Times to 1970, Washington, D.C.: 1976. Return to text

18. A tax cut financed by money creation is the equivalent of a bond-financed tax cut plus an open-market operation in bonds by the Fed, and so arguably no explicit coordination is needed. However, a pledge by the Fed to keep the Treasury's borrowing costs low, as would be the case under my preferred alternative of fixing portions of the Treasury yield curve, might increase the willingness of the fiscal authorities to cut taxes.

Some have argued (on theoretical rather than empirical grounds) that a money-financed tax cut might not stimulate people to spend more because the public might fear that future tax increases will just "take back" the money they have received. Eggertson (2002) provides a theoretical analysis showing that, if government bonds are not indexed to inflation and certain other conditions apply, a money-financed tax cut will in fact raise spending and inflation. In brief, the reason is that people know that inflation erodes the real value of the government's debt and, therefore, that it is in the interest of the government to create some inflation. Hence they will believe the government's promise not to "take back" in future taxes the money distributed by means of the tax cut. Return to text

19. Some recent academic literature has warned of the possibility of an "uncontrolled deflationary spiral," in which deflation feeds on itself and becomes inevitably more severe. To the best of my knowledge, none of these analyses consider feasible policies of the type that I have described today. I have argued here that these policies would eliminate the possibility of uncontrollable deflation. Return to text

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

https://en.wikipedia.org/wiki/Ben_BernankeBernanke taught at the Stanford Graduate School of Business from 1979 until 1985, was a visiting professor at New York University and went on to become a tenured professor at Princeton University in the Department of Economics. He chaired that department from 1996 until September 2002, when he went on public service leave. He resigned his position at Princeton July 1, 2005.

Bernanke served as a member of the Board of Governors of the Federal Reserve System from 2002 to 2005. In one of his first speeches as a governor, entitled "Deflation: Making Sure It Doesn't Happen Here", he outlined what has been referred to as the Bernanke doctrine.[35]

As a member of the board of governors of the Federal Reserve System on February 20, 2004, Bernanke gave a speech in which he postulated that we are in a new era called the Great Moderation, where modern macroeconomic policy has decreased the volatility of the business cycle to the point that it should no longer be a central issue in economics.[36]

In June 2005, Bernanke was named chairman of President George W. Bush's Council of Economic Advisers and resigned as Fed governor. The appointment was largely viewed as a test run to ascertain if Bernanke could be Bush's pick to succeed Greenspan as Fed chairman the next year.[37] He held the post until January 2006.

Chairman of the United States Federal Reserve

On February 1, 2006, Bernanke began a fourteen-year term as a member of the Federal Reserve Board of Governors and a four-year term as chairman (after having been nominated by President Bush in late 2005).

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

OCTOBER 24, 2005

Federal Reserve Chairman Announcement

President Bush announced his selection to replace Federal Reserve Chairman Alan Greenspan, whose term would expire January 31, 2006. In the Oval Office announcement attended by both the nominee and outgoing chairman, he nominated Ben Bernanke, the current president of the Council of Economic Advisers, and talked about Mr. Bernanke’s qualifications and experience in monetary policy. He also praised Mr. Greenspan for his service through several presidential administrations. Mr. Bernanke also spoke about Mr. Greenspan’s service and pledged to continue to manage the Federal Reserve in a like manner.

https://www.c-span.org/video/?189524-1/ ... nouncement

Federal Reserve Chairman Announcement

President Bush announced his selection to replace Federal Reserve Chairman Alan Greenspan, whose term would expire January 31, 2006. In the Oval Office announcement attended by both the nominee and outgoing chairman, he nominated Ben Bernanke, the current president of the Council of Economic Advisers, and talked about Mr. Bernanke’s qualifications and experience in monetary policy. He also praised Mr. Greenspan for his service through several presidential administrations. Mr. Bernanke also spoke about Mr. Greenspan’s service and pledged to continue to manage the Federal Reserve in a like manner.

https://www.c-span.org/video/?189524-1/ ... nouncement

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

These are John's comments a few days after Bernanke was nominated.

http://www.generationaldynamics.com/pg/ ... rnanke.htmBen S. Bernanke: The man without agony

Bernanke and Greenspan are as different as night and day, despite what the pundits say.

(29-Oct-2005)Summary

Ben S. Bernanke, President Bush's nominee for the new Fed Chairman, is completely different from the man he'll be replacing, Alan Greenspan. Nowhere is the difference so apparent as when you contrast Bernanke's "What me worry?" attitude toward economic bubbles with Greenspan's genuine agony over the fact that his gut is telling him that we're headed for a major financial crisis.

Possibly what bothers me most about Ben S. Bernanke is that I fail to detect in him any of the agony that has characterized Alan Greenspan’s speeches in the last year.

There are many things - race, religion, etc. - that are irrelevant to predicting how a Fed chairman will conduct policy. But the generation into which a man is born is very relevant.

We can see that right away in their policy priorities.

A generation apart

Greenspan was born in 1926, and grew up surrounded by massive starvation and homelessness in the Great Depression, so his priority at the Fed has been to contain the damage from the 1990s bubble.

Bernanke was born in 1953 and grew up during the 1950s, when America had already defeated the Depression and defeated the Nazis, and no goal was out of reach. He was in college in the 1970s when high inflation was the major problem, so naturally inflation is his highest priority policy issue today.

Bernanke doesn’t worry about bubbles, because to him those were all fixed in the 1930s, and now they always take care of themselves. In October 2002, he said:

“It’s extraordinarily difficult for the central bank to know in advance or even after the fact whether or not there’s been a bubble ... The central bank should focus the use of its single macroeconomic instrument, the short-term interest rate, on price and output stability. It is rarely, if ever, advisable for the central bank to use its interest rate instrument to try to target or control asset price movements, thereby implicitly imposing its view of the proper level of asset prices on financial markets.”

Ben Bernanke

In view of those remarks, it's not surprising that Bernanke testified to Congress's Joint Economic Committee last week that although housing prices have risen 25% over the last two years, these increases "largely reflect strong economic fundamentals," such as strong growth in jobs, incomes and the number of new households.

What, me worry?

Actually, Bernanke doesn't even think that the 1929 crash was much of anything. In October, 2000, he wrote that the crash was caused by Fed policy errors, specifically raising interest rates in the early 1930s. He wrote:

"Without these policy blunders by the Federal Reserve, there is little reason to believe that the 1929 crash would have been followed by more than a moderate dip in U.S. economic activity."

But the generational difference between Bernanke and Greenspan goes far deeper than simple policy priorities. Bernanke belongs to the arrogant, narcissistic “Boomer Generation” that humiliated Greenspan’s generation in the 1960s-70s, and forced two Presidents (Johnson and Nixon) to leave office in disgrace. This is where the Boomer generation gets its “nothing is ever my fault or my responsibility” attitude.

That explains Bernanke’s incredible remark last year that America’s exponentially increasing rate of public debt is everybody’s fault but ours, because other nations are guilty of a a "global savings glut." Only a Boomer would say something like that.

But the scariest (to me) of Bernanke’s views are the ones that economists this week have been most abundantly praising: His belief, as laid out in a speech he made on October 7, 2004, that the Fed strongly influences the stock and bond markets merely by publishing the Open Market Committee minutes earlier and more often.

This is crazy. You can read investment advice in a million places on the Internet, but I’d like to see just one place where it says, “Before deciding whether to buy this stock, check to see whether the Open Market Committee minutes have been released yet.”

I’m all for more information from the Fed, but publishing meeting minutes cannot possibly affect the markets for more than a day or so, or until the price of oil per barrel changes, whichever comes first.

Beating the Depression and the Nazis

Alan Greenspan would never (I hope) make a speech like that. He grew up surrounded by people in the G.I. generation who beat the Depression and beat the Nazis by making real sacrifices and real compromises and risking their lives. How many battles were won by releasing meeting minutes?

Boomers in general don’t realize how they’ve been protected by people in the G.I. generation and in Greenspan’s Silent Generation. In the 1980s, Democratic and Republican senators put party politics aside to agree on a plan to save Social Security, and then again to agree on a plan to reduce the budget deficit. In 1996, Democratic President Clinton compromised with the Republican-controlled Congress to eliminate the budget-draining welfare entitlement.

But those people are gone now. Republicans and Democrats from the Boomer and Gen-X generations are incapable of compromising on anything. All we get today are bitter political battles, but no important agreements or compromises. That’s why the credit markets are out of control. (Did you know that the plan to spend $2 billion on Hurricane Katrina recovery would amount to over $1 million per affected family?)

So it’s worth taking a minute to look at how the tone of Greenspan’s public statements in the last two years has been starkly different from that of Bernanke’s statements.

In January, 2004, Greenspan was quite positive and hopeful when he bragged in a speech:

"There appears to be enough evidence, at least tentatively, to conclude that our strategy of addressing the bubble's consequences, rather than the bubble itself, has been successful. Despite the stock market plunge, terrorist attacks, corporate scandals and wars in Afghanistan and Iraq, we experienced an exceptionally mild recession, even milder than that of a decade earlier." -- Alan Greenspan to the American Economic Association's annual meeting.

Greenspan began to express mild alarm at the increasingly serious economic situation in October, when he referred to the debt level and housing bubble:

“The persistently elevated bankruptcy rate remains a concern ... [but] short of a significant fall in overall household income or in home prices, debt servicing is unlikely to become destabilizing.”

These mild expressions of concern continued even through the November publication of Greg Ip’s Wall Street Journal article on Greenspan’s legacy, in which he laid out at length his detailed strategy in dealing with the 1990s bubble. The strategy was flawed, as I wrote at the time, but at least Greenspan had a strategy. (Bernanke doesn't believe that a strategy is needed.)

By January, 2005, Greenspan's statements became increasingly alarming. In one speech, he said:

"The dramatic advances over the past decade in virtually all measures of globalisation have resulted in an international economic environment with little relevant historical precedent."

A careful reading of that speech reveals that, because of unexpected globalization of the economy, Greenspan was completely repudiating the strategy that Greg Ip had described in November in the Wall Street Journal.

For some strange reason, neither Ip nor any other major financial reporter discussed this repudiation. At least Greenspan’s “conundrum” remark, referring to the puzzling worldwide fall in long-term bond rates, has been widely reported

Through 2005, Greenspan has seemed to me to be increasingly in agony, as he’s seen the stock bubble of 2000 morph into a stock bubble and a housing bubble. This was beginning to look all too familiar to him; things he hadn’t seen since his childhood. It’s not surprising that Greenspan privately told France’s Finance Minister last month that “the United States has lost control of their budget.”

His public remarks were at their starkest in his “swan song” Fed speech at the end of August.

In that speech he commented favorably on the economy’s flexibility because it encourages investor risk, but warned about the stock market and housing bubbles, and added:

"To some extent, those higher [stock and housing] values may be reflecting the increased flexibility and resilience of our economy. But what [investors] perceive as newly abundant liquidity can readily disappear. Any onset of increased investor caution elevates risk premiums and, as a consequence, lowers asset values and promotes the liquidation of the debt that supported higher asset prices. This is the reason that history has not dealt kindly with the aftermath of protracted periods of low risk premiums."

History has not dealt kindly ...

When Greenspan says that “history has not dealt kindly,” he’s referring to the 1930s Depression, and he’s telling us that he thinks it’s going to happen again. Just reading his words you can almost hear the agony in his voice, as he realizes that the horrors he suffered as a boy are going to happen again – and that he’ll be blamed for it, and that it will be his legacy.

The stock market today is priced at Dow 10,300, but the underlying book value of the market is Dow 4,500 according to my computations – and according to computations performed using a different method by analyst Adam Barth in an article appearing in the July 11, 2005 issue of Barron’s.

So the market is priced at 228 per cent of book value today, which is about where it was just before the 1929 panic. Bernanke undoubtedly believes that a new panic today wouldn't do any more harm than the 1987 panic that he's old enough to remember, but the market was at 102 per cent of book value at that time, so it's not surprising that the market recovered quickly then. A panic today would be as bad as 1929.

In his heart, Greenspan knows that. The youthful Bernanke, incredibly, doesn't have a clue.

Maybe it’s just as well. Whatever’s going to happen is going to happen, no matter what Bernanke does at this point. I don’t know if he's religious or not, but if he is religious then he might wish to start praying.

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

Higgenbotham wrote: ↑Thu May 02, 2024 11:27 amRemarks by Governor Ben S. Bernanke

Before the National Economists Club, Washington, D.C.

November 21, 2002

Deflation: Making Sure "It" Doesn't Happen Here

To stimulate aggregate spending when short-term interest rates have reached zero, the Fed must expand the scale of its asset purchases or, possibly, expand the menu of assets that it buys.

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

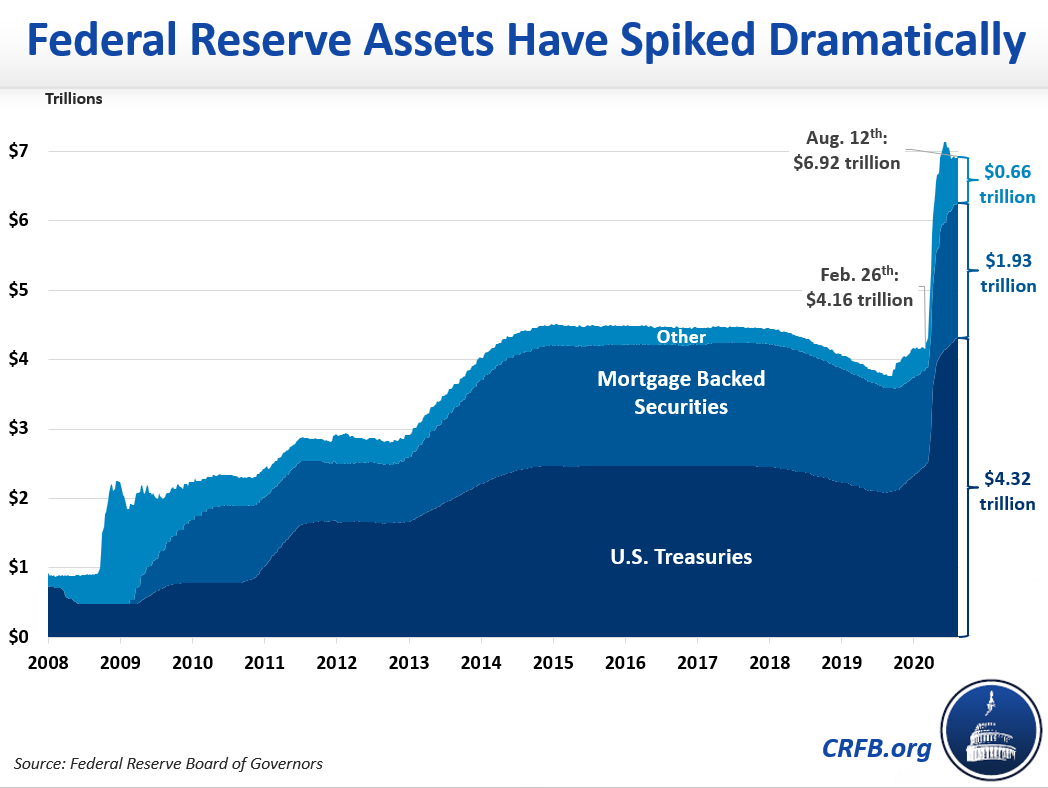

https://www.newyorkfed.org/markets/mbs_FAQ.HTMLFAQs: MBS Purchase Program

The following frequently asked questions (FAQs) provide further information about the Federal Reserve’s $1.25 trillion program to purchase agency mortgage-backed securities (agency MBS). The MBS program completed its purchases on March 31, 2010, but will continue to settle transactions over the coming months. In connection with this activity, the Federal Reserve continues to use dollar roll and coupon swap transactions to facilitate an orderly settlement of the program’s purchases.

This agency MBS program is managed by the Federal Reserve Bank of New York at the direction of the Federal Open Market Committee (FOMC). The New York Fed will continue to work with two investment managers to support the implementation of the program.

Effective August 20, 2010

General

What was the policy objective of the Federal Reserve's program to purchase agency mortgage-backed securities?

The goal of the program was to provide support to mortgage and housing markets and to foster improved conditions in financial markets more generally.

What was the volume of MBS purchased?

The FOMC directed the Desk to purchase $1.25 trillion of agency MBS. Actual purchases by the program effectively reached this target. The purchase activity began on January 5, 2009 and continued through March 31, 2010.

How were MBS purchases conducted?

MBS were purchased in the secondary market on a daily basis, with the primary dealers as counterparties. Many of these transactions were executed through external investment managers but, as described in more detail in the next paragraph, trading operations were progressively brought in-house by the Desk during the program.

Why was it necessary for the Federal Reserve to transact in the agency MBS market via external investment managers?

The operational and financial characteristics of MBS purchases are complex and require specialized technology and expertise to transact. The Federal Reserve chose external investment managers as a means of implementing the MBS program quickly and efficiently while at the same time minimizing operational and financial risks. Because of the size and complexity of the agency MBS program, a competitive request for proposal (RFP) process was employed to select four investment managers and a custodian. The selection criteria were based on the institutions' operational capacity, size, overall experience in the MBS market and a competitive fee structure. The program custodian is J.P. Morgan.

As of August 2009, the Federal Reserve streamlined the set of external investment managers, reducing the number of investment managers from four to two. The New York Fed retained Wellington Management Company, LLP for trading, settlement and as a secondary provider of risk and analytics support; and BlackRock Inc. as the primary provider of risk and analytics support.

Beginning on March 2, 2010, the New York Fed began to use internal staff to execute MBS purchases. Subsequently, the Desk alternated trading days with Wellington before assuming full trading responsibilities by program end. Dollar roll transactions since March 31, 2010 have been executed exclusively by the Desk. For the settlement of legacy purchase and new dollar roll and coupon swap transactions, the New York Fed continues to leverage the middle office settlement support of Wellington.

Why does the Federal Reserve continue to transact in agency MBS dollar rolls and coupon swaps following the completion of program purchases?

The Federal Reserve uses agency MBS dollar rolls as a supplemental tool to address temporary imbalances in market supply and demand. A dollar roll is a transaction conducted at market prices that generally involves the purchase or sale of agency MBS for delivery in the current month, with the simultaneous agreement to resell or repurchase substantially similar (although not necessarily the same) securities on a specified future date. A coupon swap is a transaction conducted at market prices that involves the sale of one agency MBS with the simultaneous agreement to purchase a different agency MBS. Coupon swaps are transactions that allow the Federal Reserve to sell agency MBS that are not readily available for settlement, and purchase different agency MBS that are more readily available for settlement. Although purchases were completed at the end of March 2010, the Federal Reserve continues to use both dollar roll and coupon swap transactions to facilitate an orderly settlement of the agency MBS program’s remaining forward purchase commitments.

With whom does the Federal Reserve transact agency MBS dollar rolls and coupon swaps?

The New York Fed transacts agency MBS dollar rolls and coupon swaps only with primary dealers who are eligible to transact directly with it.

How are Federal Reserve’s agency MBS holdings reported?

Balance sheet items related to the agency MBS purchase program are reported after settlement occurs on the H.4.1. statistical release titled "Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks." Securities acquired in dollar roll or coupon swap transactions are also included with other holdings of agency MBS. Trade settlements may occur well after trade execution due to agency MBS settlement conventions. This report also includes information on total outstanding commitments to buy and sell MBS in a supplemental table.

In addition, the New York Fed publishes the most recent weekly SOMA agency MBS dollar roll transaction activity in more detail on its external website on a weekly basis. As of October 1, 2009, consistent with New York Fed's regular practice of publishing detailed data on other SOMA holdings, such as Treasury and agency debt securities, the New York Fed also began publishing on a weekly basis detailed data on all settled SOMA agency MBS holdings. Any change in the composition of these reported holdings over time is a function of paydowns, and the program's dollar roll and coupon swap activity.

Why have there been sales from the Federal Reserve's portfolio?

As the Desk conducts agency MBS dollar rolls or coupon swaps, the Desk simultaneously buys and sells agency MBS securities. These transactions are consistent with the Desk’s directive to purchase $1.25 trillion in agency MBS, and only affect the timing and composition of the settlement of those purchases.

Will agency MBS dollar rolls or coupon swaps reduce the amount of total purchases?

No. Dollar rolls and coupon swaps, though they have certain different characteristics, are generally the simultaneous sale and purchase of the same face amount of agency MBS. Thus they only affect the timing and composition of the settlement of the Federal Reserve’s agency MBS purchases.

What will be the Federal Reserve’s investment strategy for agency MBS going forward?

On August 10, 2010, the FOMC directed the Desk to keep constant the Federal Reserve’s holdings of securities at their current level by reinvesting principal payments from agency debt and agency MBS in longer-term Treasury securities. As a result, agency MBS holdings will decline over time. Any future decisions about the investment strategy to be employed will be made by the Federal Open Market Committee.

Where should questions regarding the MBS purchase program be directed?

Questions regarding the MBS program should be directed to the New York Fed's Public Affairs department: 212-720-6130.

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

-

Higgenbotham

- Posts: 7810

- Joined: Wed Sep 24, 2008 11:28 pm

Re: Higgenbotham's Dark Age Hovel

https://www.reuters.com/markets/us/fed- ... 023-01-23/Fed needs mortgage-backed securities exit plan 'earlier than later,' George says

By Howard Schneider

January 23, 202312:36 PM CST

WASHINGTON, Jan 23 (Reuters) - Kansas City Federal Reserve President Esther George has urged her colleagues to come to terms "earlier than later" on a plan for the U.S. central bank to exit the mortgage-backed securities (MBS) market and be more explicit on how bond purchases will figure into future monetary policy.

"You can't just wake up one day and say, 'hey, we're going to get out of this business,'" George, who is retiring from her position at the end of this month, told Reuters in an interview published on Monday.

She noted that Fed officials agree in principle that the central bank's securities portfolio should only include those assets issued by the U.S. Treasury - not those backed by home mortgages - but don't yet have a plan to get there.

The Fed currently holds about $2.6 trillion of MBS as part of its roughly $8 trillion securities portfolio. That is about a quarter of the total MBS market, what George referred to as an "enormous" share that raises questions about the appropriate extent of the central bank's presence.

George, whose last day before retiring is Jan. 31, will not participate in the Jan. 31-Feb. 1 policy meeting. She spoke to Reuters before the start last Saturday of the "blackout" period that restricts Fed officials from making public comments about policy in the run-up to meetings.

The Fed is trying to reduce its balance sheet overall as part of the plan to tighten monetary policy, and is allowing up to $60 billion a month in Treasury securities and $35 billion in MBS to mature and "run off" from its holdings.

In theory, that puts upward pressure on long-term interest rates by lowering demand for those assets.

But, in the case of MBS, high interest rates also slow the pace of the run-off since it discourages both the home sales and the refinancings that, because existing mortgages get paid off, decrease the principal of MBS quicker than would occur only through monthly payments by homeowners.

'NOT IN MY DNA'

Since the Fed began to let its balance sheet decline in June, its MBS holdings have fallen by about $67 billion, or roughly 2.5%, a pace that would leave the central bank in the mortgage market for years to come. Several Fed officials have said the central bank will eventually need to sell its MBS holdings.

George said she did not have a specific plan in mind, but felt her colleagues should get to work on one.

"At some point people will have to address: is that the footprint we want in the mortgage market?" George said of the current holdings. More important than the details of any plan "is just to say how will we go about doing that earlier rather than later. There could be many combinations of things that get you there."

George, 65, has been head of the Kansas City Fed since October 2011. She has been among the central bank's more frequent dissenters, and a particular skeptic of both quantitative easing - the use of bond purchases to support markets and the economy - and the 2% inflation target adopted shortly after her arrival.

"I've never felt comfortable saying we should want inflation. It's not in my DNA," said George, whose roots are in Midwestern family farming, an industry that was particularly damaged by the high-inflation, high-interest-rate environment of the 1970s and 1980s.

While the periphery breaks down rather slowly at first, the capital cities of the hegemon should collapse suddenly and violently.

Who is online

Users browsing this forum: No registered users and 1 guest